LOS ANGELES, Calif — From Advil to Band-Aids, healthcare costs add up quickly. While budgeting for the unexpected may seem like an impossible task, financial experts say health savings accounts can be a game changer— saving you money now and later.

“It’s just an emergency savings bucket for healthcare.”

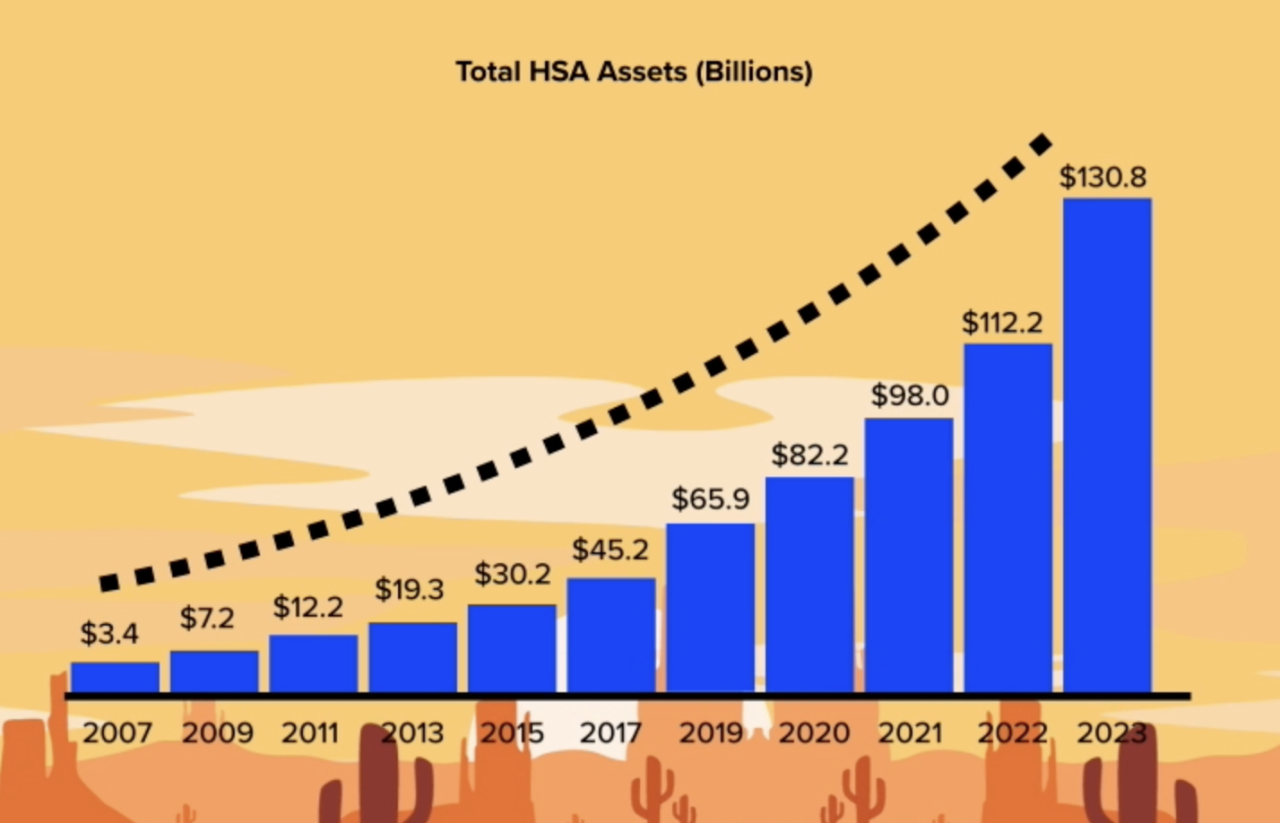

The money these accounts hold is growing. Introduced just 20 years ago, HSAs now hold more than $100 billion. That’s up from just $3.4 billion in 2007.

Cassandra Rupp is a Senior Financial Adviser for Vanguard. She says HSAs are also growing in popularity as a tax-free savings vehicle.

One of the top perks for using an HSA is less taxes now and later.

Triple Tax Benefit

Rupp says every time you contribute, you’re reducing your taxable income. Second, all investment growth is tax deferred. Then third, if you need to use the savings, you can.

“When you take a withdrawal,” Rupp says. “If it’s for qualified medical purposes, then that’s going to be tax-free.”

Flexibility

Another perk: flexibility. You can use your HSA money for short or long-term savings. That means, if you need to spend it now, you can do that with no issues, with the account functioning as an emergency savings account. In addition, that money may cover more things than you expect.

“There’s a lot,” Rupp says. “From over-the-counter medications to Band-aids and first aid to Medicare premiums and long-term care insurance.”

If you can wait to spend the money, you can expect a big payoff down the line. Spending out-of-pocket for healthcare expenses will allow you to maximize any tax-deferred growth in the account.

For example, if you pay for your child’s braces out-of-pocket and save the receipt, you can withdraw that amount later to pay for any expense. That includes things like your own retirement or college tuition for your children.